With tanks full around the world, we decided to offer a brief respite from the detailed version of the Ciatti Global Market Update. If you are reading this in the Southern Hemisphere we hope you are settling in for a nice winter as the wines finish and ready themselves for sale. If you reside in the Northern Hemisphere we hope that you are well rested from your summer vacations and ready for an eventful harvest season.

With tanks full around the world, we decided to offer a brief respite from the detailed version of the Ciatti Global Market Update. If you are reading this in the Southern Hemisphere we hope you are settling in for a nice winter as the wines finish and ready themselves for sale. If you reside in the Northern Hemisphere we hope that you are well rested from your summer vacations and ready for an eventful harvest season.

This Coffee Shop article is an excerpt from the Ciatti Global Wine Grape Brokers’ August, 2014 Global Market Update (Volume 5 Issue No. 8). Here, we focus on the California and USA section of the report. See the full report for global wine market update for countries including Argentina, Australia &New Zealand, Chile, France, Germany, Italy, South Africa, and Spain.

In the following pages, we hope that our direct and to the point, albeit abbreviated country comments will offer you some quick insight into the market as we see it today. As an added bonus however, Greg Magill has taken this opportunity to do a country by country round up of the World of Concentrate. We would like to thank you all for being loyal readers, and will bring you a full and detailed report in September.

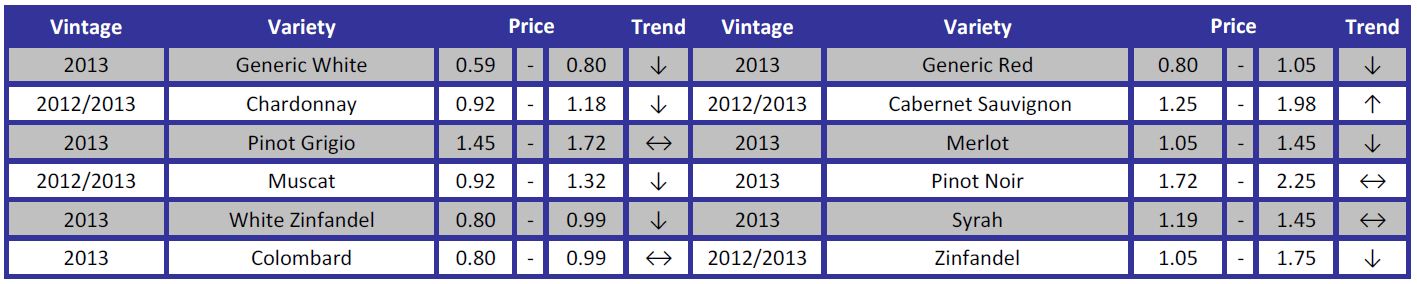

Export Pricing: USD per liter. Currency Conversion Rates as of August 11, 2014

California – wine

After the large 2012 and 2013 harvests, many were speculating that California grapevines would take a break and give a lower yield in 2014. Harvest has now begun in the Southern San Joaquin Valley and the harvest looks reasonable at this point. Some grape varieties are showing moderate yields, but it is VERY early to make any sort of predictions just yet. California wineries that offer storage contracts had a brisk season, and there is virtually no space available as the crop starts coming off the vine. While the Central Valley may offer a slight respite from the past large harvests, the Coastal regions still look very good in terms of yield. Both the Central Valley and the Coast are showing excellent quality, with limited disease pressure in any area. Although the 2014 harvest looks very promising at this point, the drought remains top of mind as growers look to 2015 and beyond.

USA – White Concentrate

The generic grape crop for concentrate could be 20‐25% shorter than last year’s crop. Demand for domestic WGJC has waned over last year, mainly due to the lack of demand from both the wine and food and beverage industries. Raisin demand, however, has been rock solid ‐ if a farmer can lay his crop down, he most certainly will. While pricing for the 2014 generic grape crop has yet to be established, both domestic and international carry‐over stocks will keep downward pressure on this market. The problem being witnessed is that the high cost of domestic farming and severe lack of water and lower yields helped along by this drought, will cause more acres to be ripped from the ground after this harvest. Several farmers are lining up to continue the pullouts, in favor of saving and/or replanting for more economically sustainable crops in the valley.

USA – Red Concentrate

There are mix reports regarding the Rubi Red crop at this time. Some are saying that the crop looks large, while others are taking a much more cautious approach, as the crop has yet to show size or color potential, due to severe drought conditions. The amount of water and quality of water available to the farmers is an important factor. An estimated 90% + of this crop is committed to long‐term planting contracts, so price fluctuations are not expected.